1. Context/Background

What is a ZEV mandate?

The transport sector produces the greatest share of UK domestic greenhouse gases (GHGs) and has seen relatively little change since 1990 while emissions from other sectors (such as energy and business) have steadily fallen. Cars and vans alone were responsible for 18% of the UK’s total domestic GHG emissions in 2021.

A Zero-emission Vehicle (ZEV) mandate requires manufacturers to sell an ever-increasing percentage of zero-emission machines such as electric cars.

The Government state that having a minimum percentage of manufacturer new car and van sales be zero emission each year from 2024 will ensure their future supply and provide certainty to chargepoint operators and energy suppliers to coordinate the necessary investments in new technology and infrastructure.

2. Policy

Governments new net zero plan called “Powering up Britain”

The government was forced to publish this strategy after the High Court judged last July that its current plan was not detailed enough to show how the UK would meet its goal to reduce its greenhouse gas emissions to net zero by 2050.

The ZEV mandate will be the lever to deliver legally required reductions in carbon emissions from light-duty road transport. This will set the minimum annual targets for the percentage of new car and van sales that must be zero emission. Each year, manufacturers will receive allowances to sell non-ZEV vehicles up to a given percentage of their fleet of new cars and vans, with the intention that ZEVs account for the remainder of sales. Any excess non-ZEV sales must be covered by purchasing allowances from other manufacturers, by using allowances from past or future trading periods (banking or borrowing) during the initial years of the policy or by offsetting with credits.

This starts from 1 January 2024 for the UK, reaching 100% in 2035. The ZEV mandate is a fundamental shift in how the UK regulates CO2 emissions from new cars and vans and will distinguish us from the European Union.

Brief overview:

• Only vehicles with a zero-emissions range of over 120 miles will be covered by the mandate.

• Smaller-scale OEMs which sell less than 2,500 vehicles a year will remain exempt from the legislation until 2029.

• Banking of ZEV allowances will be allowed, subject to some limits and restrictions.

• Borrowing of ZEV allowances will be allowed between 2024 to 2026, subject to caps on the amount that can be borrowed and with interest payable on the deficit.

• To qualify as a ZEV, new cars and vans will need to meet certain minimum eligibility criteria. Manufacturers can earn additional credits for deploying ZEVs for use in specific applications, such as car clubs.

• During the years 2024 to 2026, any overachievement against the minimum requirements of the new non-ZEV CO2 emission targets can be used to offset non-compliance with the ZEV mandate, though this will be capped.

Please find NFDA’s latest Press Release on the Government’s Powering up Britain announcement here.

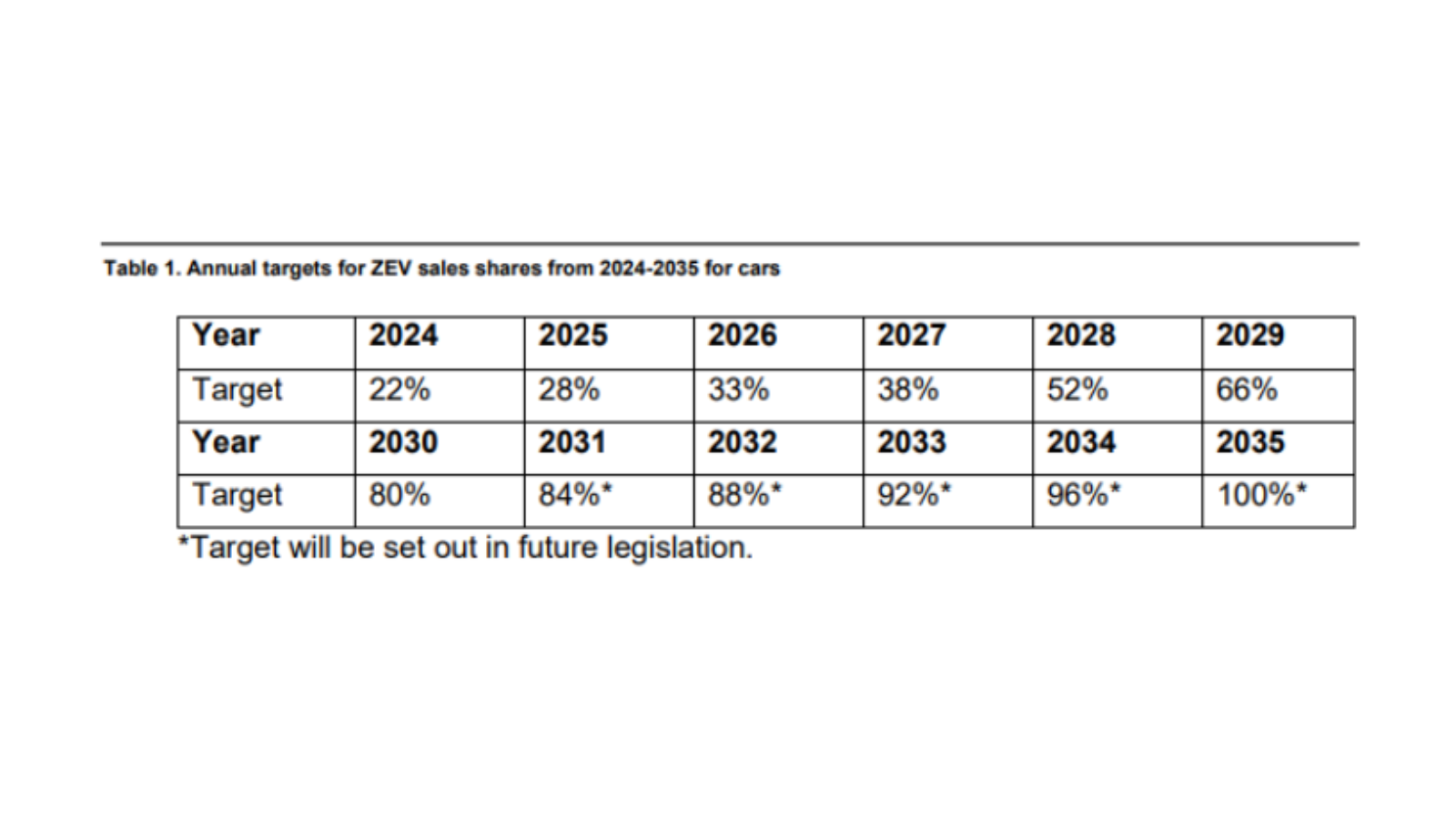

Cars:

The proposed minimum ZEV target trajectory for new cars sold begins at 22% in 2024, increasing to 80% in 2030 and reaching 100% in 2035.

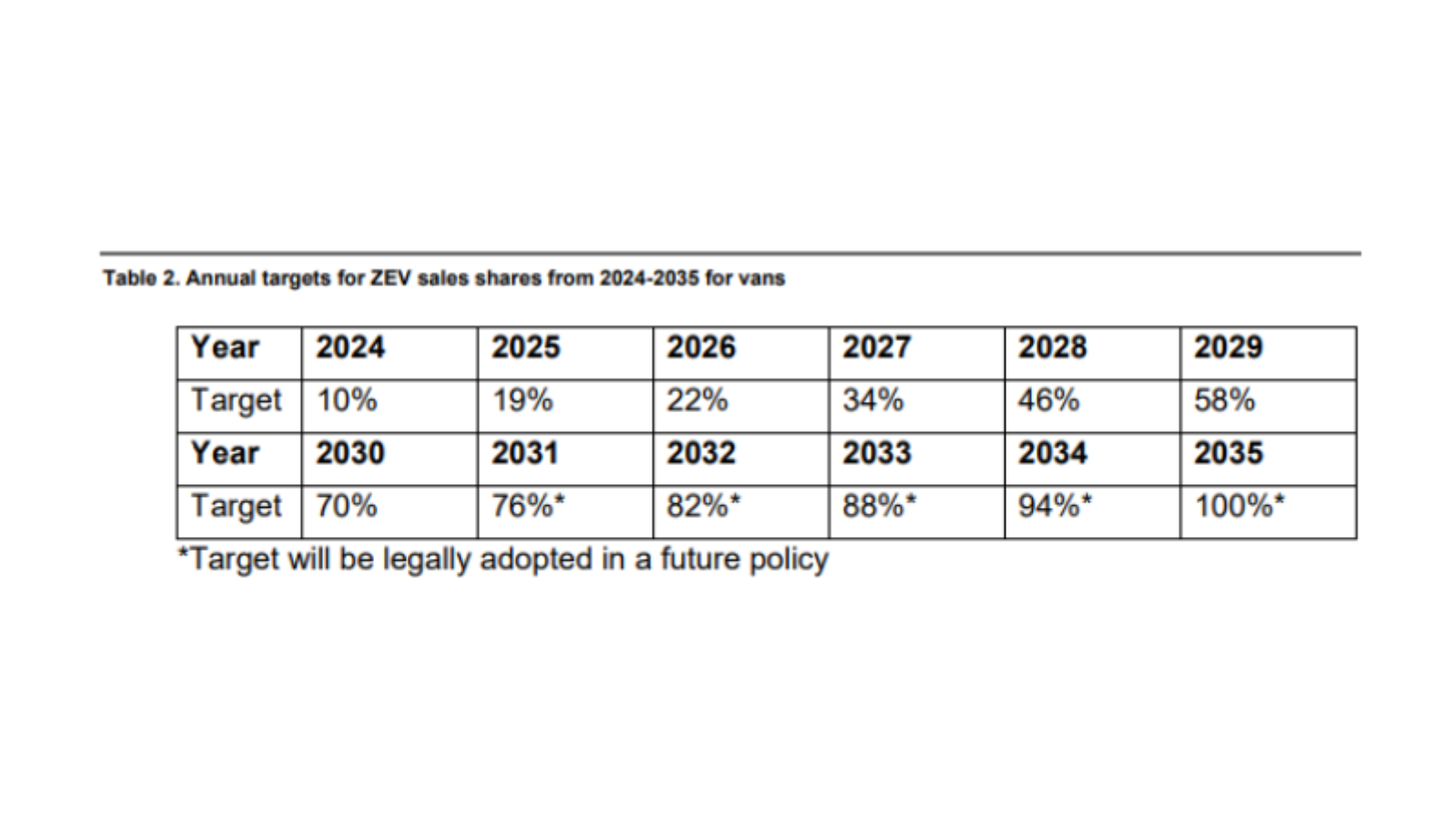

Vans:

The proposed minimum ZEV target trajectory for new vans sold begins at 10% in 2024 and reaches 70% in 2030 on the way to 100% in 2035.

If manufacturers exceed their ZEV targets, excess ZEV mandate allowances may be traded freely to other manufacturers for any price. These allowances will be capped and decline each year.There will be some additional flexibilities during the initial phase of the regulation. Between 2024-2026, manufacturers may borrow a limited number of ZEV allowances from future periods if they are unable to achieve compliance from their sales.

However, the number that may be borrowed is capped and will decline each year: 75% of the target may be covered by borrowing in 2024, 50% in 2025 and 25% in 2026. Furthermore, any borrowing must be repaid with 3.5% annual interest to maintain carbon savings. Beginning in 2027, borrowing from future trading periods would not be allowed, and participants’ deficits must be repaid by the end of 2027.

Unused allowances may be banked for use in future years. This flexibility will extend at least until the end of 2030, but banked allowances will expire if not used after 3 years to ensure that sufficient ZEV allowances are available for effective trading.

If manufacturers cannot meet compliance through in-year allocated allowances, banked or borrowed allowances, allowances purchased from other manufacturers through trading, or bonus credits, they must make a payment to government. The proposal suggests payments of £15,000 per non-ZEV car and £18,000 per non-ZEV van registered which is not covered by allowances.

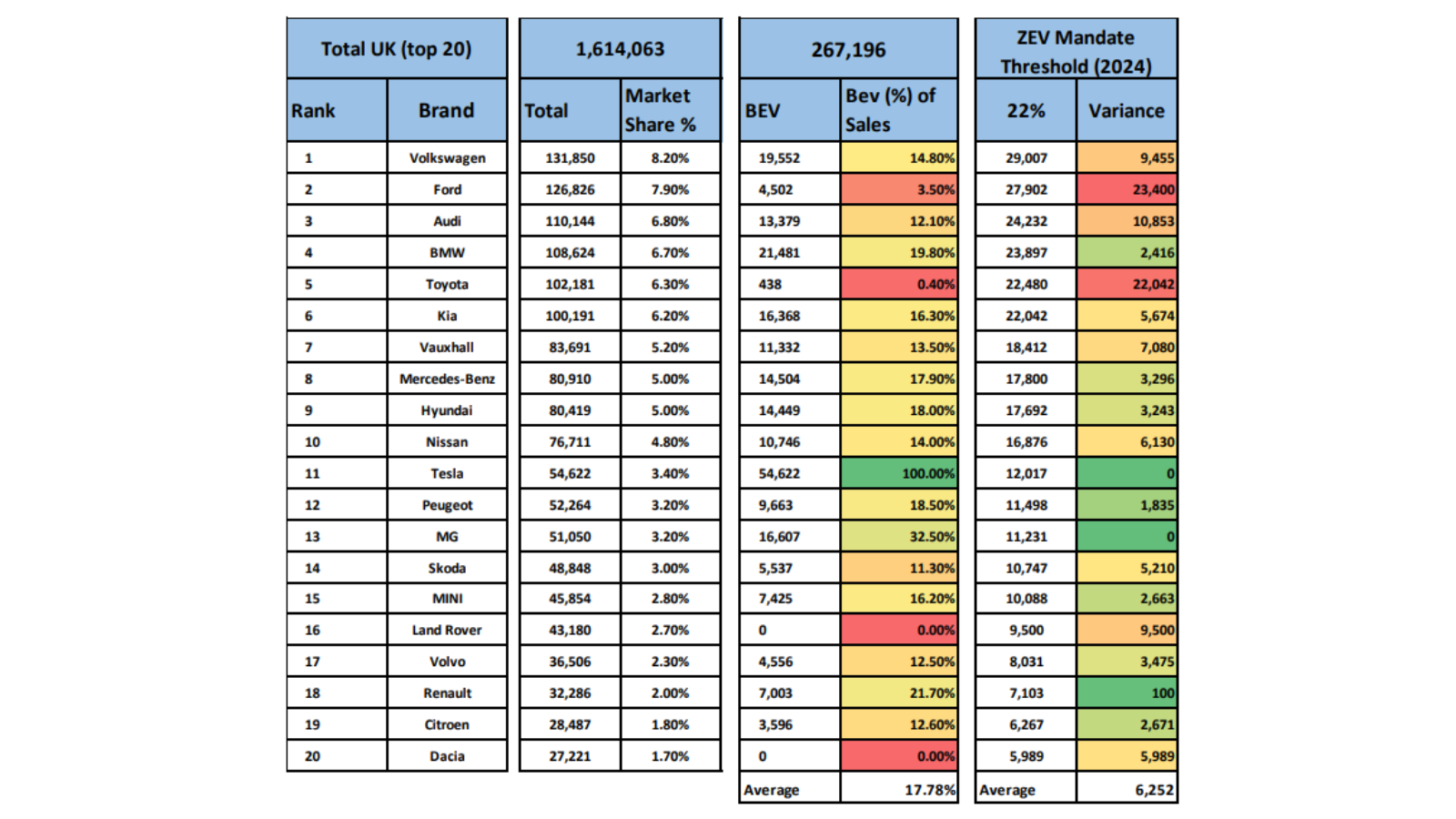

3. Current OEM comparison -

If the ZEV mandate was to be applied to the above 2022 new car reg data, only two (Tesla and MG) out of the top 20 brands would have surplus ZEV credits. Overall, the top 20 brands were under their ZEV qualifying by an average of 6,252 vehicles, equating to an expenditure of £93.8M per manufacturer under an assumption of the per vehicle £15,000 penalty or between £46.9M and £62.5M (at £7,500 and £10,000 pv respectively) when the open trading of credits commences.

Winners –

Tesla registered 54,622 cars in 2022. 100% of those qualify as ZEVs. Therefore, if the 22% target had applied in 2022 they would have amassed a total of 12,016 credits. As Tesla only sells EVs, the only value to these credits is selling them on the open market to another OEM who cannot achieve 22% ZEV registrations. On the basis that fines for non-compliance are being suggested at c£15,000 for non-ZEV qualifying units then Tesla could reasonably expect to command a value for these credits>£10,000. £10k free cash to either further discount their product or take to the bottom line. That’s £120m for simply continuing their business sales model.

Polestar registered 7345 units last year which was a good entry into the market and with more products coming they look set to grow. They can benefit similarly to Tesla but as Polestar is owned by Geely, they may elect to utilise credits to offset any target miss by sister brand Volvo. An in-house trade that helps sustain both brands competitive position.

Losers –

Ford has long been the market leader in new car sales and whilst Volkswagen has recently usurped that position the blue oval has been by far the most popular brand in the UK for decades. They registered 126,826 units last year but with only Mach-E as a qualifying ZEV their percentage ZEV share is extremely low. More Ford BEVs will arrive in late 2023 but they are in “catch-up” mode and have a huge gap to close in order to meet the 22% target in 2024.

Ways a manufacturer can meet the 22% ZEV qualification target:

1. Enter the open market and buy credits from other OEMs who possess a surplus. However, erodes profits and supports a competitor.

2. Manufacturers have a three-year period ending on December 31, 2026, where they can purchase credits from the Government, however, this comes with a 3.5% interest penalty on per credit purchased.

3. They can pay a penalty of £15k a bonnet, which would wipe out any potential for market profitability.

4. Can reduce overall volume aspirations so the ZEV qualifying sale is reduced and thus becomes more achievable.

Impact on Dealers -

Dealers are at the mercy of their OEM partners. The strategy to align with OEMs who have a clear electric vehicle strategy will now look more appealing to dealer groups as the volumes and competitive positioning are more assured, but no one knows for sure what the next 3-4 years will bring other than to say – expect the unexpected and have contingency plans.

European comparison -

The ‘Fit for 55’ deal will end the sale of new CO2-emitting cars in Europe by 2035.9 As an intermediary step towards zero emissions, the new CO2 standards will also require average emissions of new cars to come down by 55% by 2030, and new vans by 50% by 2030, compared to1990 levels.

Germany won an exemption to create a legal route for sales of new cars that only run on e-fuels to continue after 2035.10 E-fuels are considered carbon neutral because they are made using captured CO2 emissions – which proponents say balance out the CO2 released when the fuel is combusted in an engine. E-fuels are not yet produced at scale. You can find NFDA’s preliminary opinion on E-fuels here.

The Commission will, in autumn 2023, propose how sales of e-fuel-only cars can continue after 2035.

Such cars will have to use technology to prevent them from starting when filled with petrol or diesel.

4. Future

New consultation:

The new and final consultation will be seeking views on the ultimate design of the UK’s Zero Emission Vehicle mandate and C02 emissions regulation for new cars and vans. The legislation being proposed will cover ZEV and non-ZEV requirements in the 2024-2030 period. Legislation covering the 2031-2035 period will be introduced at a later point, but it is intended that the legislative minimum trajectories will be at least as ambitious as set out in current trajectories.

Non-ZEV CO2 emissions standard overview

The goal of this new regulatory framework is to support the rapid shift toward ZEVs and provide market certainty for the automotive, chargepoint and energy sectors and their supply chains.Additional research and development into further incremental improvements to combustion engine efficiency technologies is no longer a key objective.

The framework includes a CO2 emissions standard applied to new non-ZEV cars and vans to ensure they do not become less efficient and more polluting over time.

Details still yet to be defined:

The final proposals are currently being consulted upon in this new consultation. These involve:

1. the level of ZEV uptake (trajectories)

2. how allowances and credits could be allocated and used

3. flexibilities including banking, borrowing and transfers between schemes

4. derogations and exemptions

5. how to regulate the non-ZEV portion of the fleet

6. how the ZEV mandate and non-ZEV CO2 regulation interact

The consultation will close on 24 May 2023; a link can be found here.